I read a few other substacks recently with folks looking at some foreclosure and home equity data that would suggest we are not heading for the kind of meltdown we saw in the great recession. I think that if they looked at it a little more from my admittedly dark perspective, they might question some of the assumptions there, even just anecdotally. I mean, just this week alone I’ve laid out $2.4 Million in mortgage fraud for you…and it’s only Thursday morning!!!

One argument is that home equity numbers are much higher now. Well, yes, we have let the ponzi get a little more out of control this time, haven’t we? I would argue those equity numbers are falsely inflated, and I would also question whether they are taking all of the other kinds of LOC’s and record consumer debt/judgments into account. Also, wasn’t home equity pretty high when the market was super-heated in 2006/2007? The problem might be that you are looking at the home equity of ALL of us (including those that own their homes or haven’t used their homes as an ATM), while meltdowns begin at the margins.

Another argument is that everyone has a sweet fixed 30-year rate and is just going to sit on it for 30 years. Maybe, but let’s just say the lenders wanted to get out of all of these low-rate long-term mortgages just with the people that fibbed about occupancy on their mortgage applications??? I also think there is an underestimation of how many people will be forced to sell or walk away. Just in my limited sample we can see some panic selling and underwater rentals, and that would/could include today’s suspect!

Today we have a guy that lives in Florida with a couple of Scottsdale rental properties worth nearly $2 Million and leveraged to the hilt. And of course, he said he was going to live in one of them, and then a few days later changed his mind and rented it out. Now, if you were a lender locked into a 30-year mortgage at 3% with this dude, wouldn’t you demand your money back yesterday so you could reinvest it risk free at 5%!? If I was Guaranteed Rate, I would certainly demand it back! (Alaska USA can and will pound sand!).

Suspect - Emiliano Diez (DOB 4/1/1975).

Scottsdale Income Property 1 - On September 20th, 2022, Mr. Diez acquired 16215 N. 63rd Pl., Scottsdale AZ 85254 for $1,000,000. This was financed by a $600,000 30-year mortgage from Guaranteed Rate, Inc. AND a $299,000 2nd mortgage from Alaska USA Federal Credit Union. Owner Occupancy is a covenant of the first mortgage (and likely the 2nd as well given he willfully lied on the first…). In both Deed Trusts, Mr. Diez states that he resides at 821 E. Village Cr, Davie Florida, 33325. The property was listed for rent for $5000/month on September 24th, 2022. The property is currently classified as a Primary Residence by the Maricopa Assessor.

Scottsdale Income Property 2 - On March 26th, 2019, Mr. Diez acquired 8506 N. Timberlane Dr., Scottsdale AZ 85258 for $740,000. This was most recently financed by a $690,000 30 year mortgage taken out with TruWest Credit Union on May 20th, 2020 and a $300,000 LOC taken out on August 19th, 2021 from TruWest Credit Union. The home was registered as a rental with Maricopa County on October 6th, 2021. Mr. Diez lists his Florida address in the LOC deed trust. The property was listed for rent in March of 2023 for $8000/month.

Rental of Scottsdale Income Property 1 - Per a number of sources the home is rented to a Peter and Amy Costas.

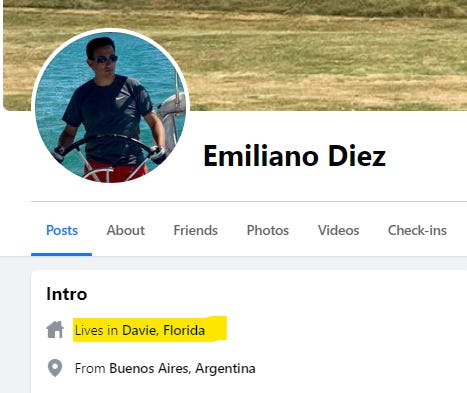

Principal Residence - As above and in social media, Mr. Diez admits to living in Florida. https://www.facebook.com/emiliano.diez/

Mortgage Occupancy Fraud - With respect to Income Property 1…obvious. Income Property 2 is probably fine, though I would question whether this isn't a financial disaster waiting to happen, even without the federal proceedings that should come of this? Mr. Diez has nearly $2 Million in debt on a couple of rental homes where I sincerely doubt the lenders could recover their funds if they had to right now…